How to Choose the Best Horse Insurance

Search "best horse insurance" and you mostly get lists. The truth is the best policy is the one that fits your horse, your budget, and your peace of mind — you just need to know what to compare. This owner-friendly checklist walks you through it all: coverage that matches how you ride (including colic), the freedom to use any vet, the real cost after deductible and co-pay, how fast claims are paid, renewal terms, and the people behind the policy.

Search "best horse insurance" and you'll get a dozen confident answers — and most of them are really just lists. The truth is, the best horse insurance isn't a single company; it's the policy that fits your horse, your budget, and your peace of mind. The trick is knowing what to compare so you can spot it.

Here's an owner-friendly checklist for choosing coverage you'll actually be glad you have when it matters.

1. Start with the right coverage, not the lowest price

The cheapest policy isn't a bargain if it doesn't cover the thing that goes wrong. Before you compare prices, get clear on what you need:

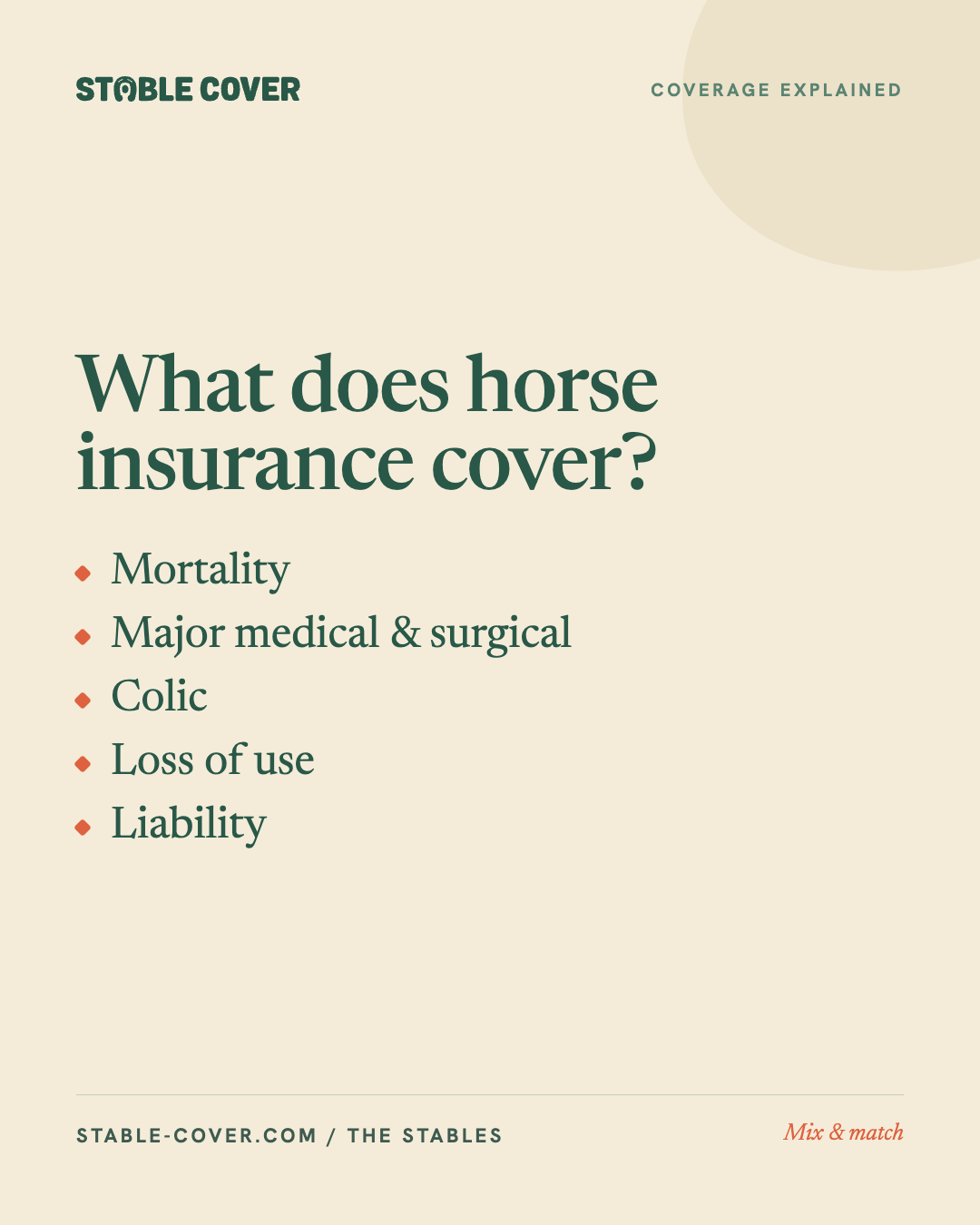

- Mortality to protect your horse's value

- Major medical and surgical for vet bills and operations

- Colic coverage specifically (it's common and expensive — surgery often runs $7,000–$15,000)

- Loss of use if your horse has a job

- Liability if you want to protect yourself, too

Match coverage to how you ride and what you couldn't easily pay out of pocket. Not sure what each type does? Our guide to what horse insurance covers breaks it down.

2. Check if you can use your own vet

This is a big one that's easy to miss. Some policies steer you toward certain providers. The best coverage lets you use any licensed vet you trust — which matters enormously in an emergency, when you want your own vet and the nearest surgical facility, not whoever's in a network. (With Stable Cover, any licensed U.S. vet works.)

3. Look at the deductible and the co-pay

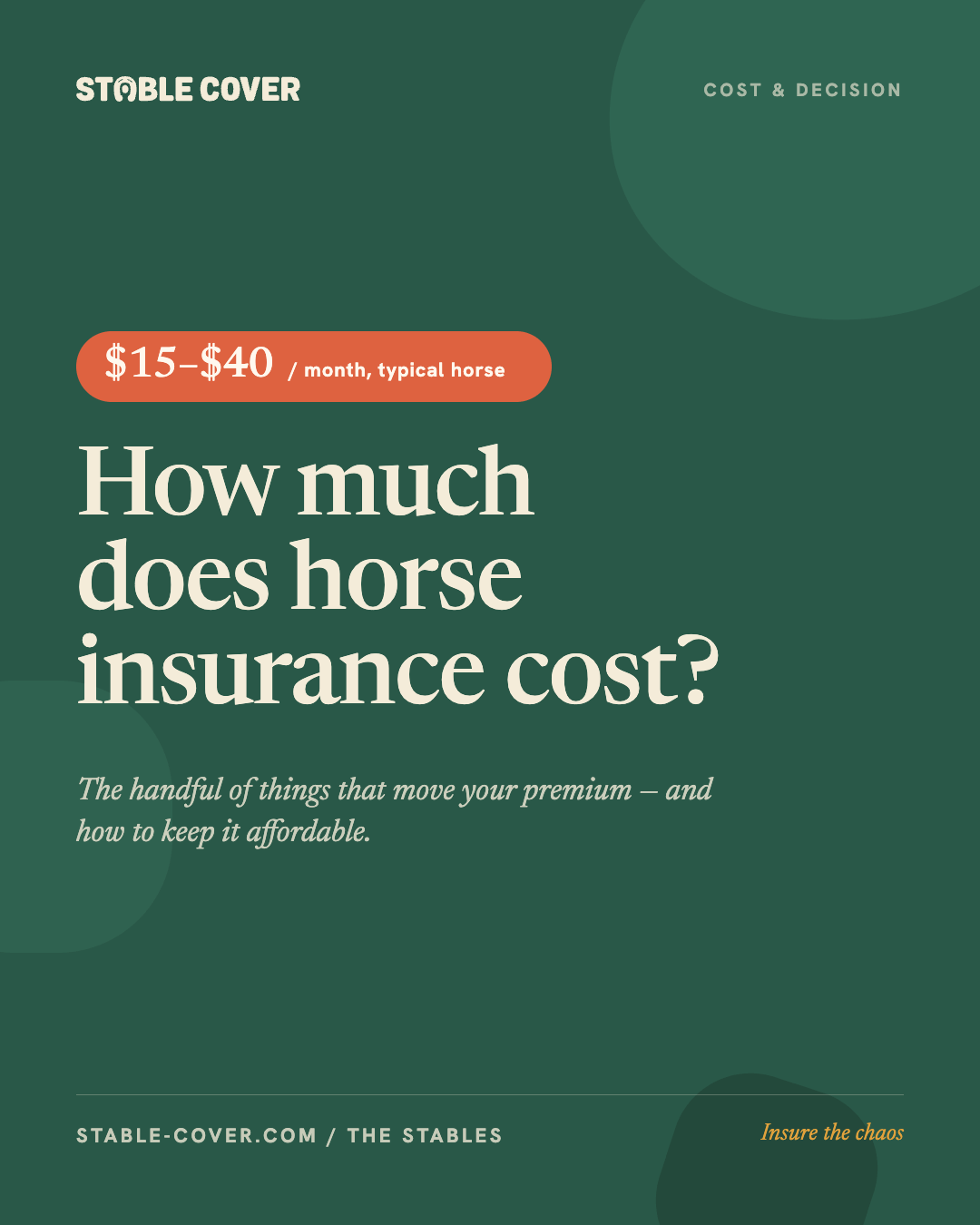

A low monthly price can hide a high cost at claim time. Two numbers tell the real story:

- Deductible — what you pay before coverage kicks in

- Co-pay — the share of the bill you keep paying after that

A policy with $0 deductible and 0% co-pay options can mean far more of your bill comes back to you than a "cheaper" plan with high out-of-pocket costs. Always compare the whole picture, not just the premium.

4. Ask how fast claims are paid

Insurance is only as good as its claims experience. When you've just covered a hospital stay, waiting weeks for reimbursement hurts. Ask each provider how long claims take. (For reference, most Stable Cover claims are reimbursed within 48 hours of approval.)

5. Check the renewal terms

Some policies make you re-apply every year — which can mean new conditions getting excluded at renewal. Automatic renewals keep your coverage continuous, so a problem that develops mid-policy doesn't become a reason to drop you later. It's a quietly important detail.

6. Look at financial strength and who's behind the policy

You want to know the company will be there when you file a claim. Look for established underwriting and a provider that's transparent about who they are and where they're licensed. (Stable Cover is licensed in 30+ states across the U.S.)

7. Judge the support before you're a customer

You can learn a lot from how a company treats you before you buy. Are you talking to a real person or a chatbot? Do they explain things clearly or bury you in jargon? The best horse insurance comes with people who actually understand horses — because someday you'll be calling them on a hard day.

A quick checklist to compare providers

When you're weighing your options, score each one on:

- ✔️ Does it cover what my horse actually needs (including colic)?

- ✔️ Can I use any licensed vet?

- ✔️ What's the real cost after deductible and co-pay?

- ✔️ How fast are claims paid?

- ✔️ Does it renew automatically?

- ✔️ Is the provider established and licensed in my state?

- ✔️ Do I get real, knowledgeable support?

If a policy checks those boxes at a price that works for you, you've found your best horse insurance — whatever the listicles say.

See how Stable Cover measures up

We built Stable Cover around exactly this checklist: any licensed U.S. vet, $0 deductible and 0% co-pay options, most claims reimbursed within 48 hours, automatic renewals, and real support from people who ride. Compare for yourself on our best horse insurance page, see what coverage costs, or request a quote and we'll help you find the right fit — no pressure, no bots.

Frequently Asked Questions

What is the best horse insurance?The best horse insurance is the policy that matches your horse's needs and your budget — not a single company. Compare coverage (including colic), the freedom to use any vet, deductible and co-pay, claims speed, renewal terms, and the provider's financial strength to find your best fit.

What should I look for in horse insurance?Look for coverage that fits how you ride, the ability to use any licensed vet, low deductible and co-pay options, fast claims, automatic renewals, and an established, licensed provider with knowledgeable support.

Does the cheapest horse insurance save money?Not always. A low premium can come with a high deductible and co-pay, meaning you pay more at claim time. Compare the full cost of a claim, not just the monthly price.

How do I compare horse insurance companies?Use a consistent checklist: coverage match, vet freedom, deductible and co-pay, claims speed, renewal terms, financial strength, and quality of support. Scoring each provider the same way makes the best choice clear.

Popular Posts

Strangles Awareness Week 2025

Understanding Pre-Existing Conditions

The Ultimate Guide to Equine Physical Therapy

The Stable Categories

Your horse's protection, tailored to complement your lifestyle effortlessly.